While most cryptocurrency traders focus on candlestick patterns and popular technical indicators, a sophisticated subset of traders quietly profits from analyzing order book imbalances—a powerful yet underutilized approach that reveals the true supply and demand dynamics hiding beneath the surface of market prices.

Order book imbalance trading represents a microstructure-based strategy that examines the relationship between buy and sell orders at various price levels to predict short-term price movements. This approach goes beyond simple price action analysis by incorporating the actual intentions of market participants as expressed through their limit orders. Unlike conventional trading methods that react to price movements after they occur, order book analysis allows traders to anticipate potential price changes before they materialize.

The cryptocurrency market, with its 24/7 operation and relatively transparent order book data across multiple exchanges, provides an ideal environment for implementing these strategies. However, the complexity of properly analyzing order flow data and the technical requirements for implementation have kept this approach largely within the domain of institutional traders and sophisticated algorithmic trading firms.

- The Anatomy of Cryptocurrency Order Books

- Depth Visualization and Market Psychology

- Defining and Measuring Order Book Imbalance

- The Mathematics of Imbalance

- Advanced Imbalance Metrics

- Temporal Dynamics of Imbalance

- Implementing Order Book Imbalance Strategies

- Strategy Development Framework

- Real-Time Signal Generation

- Multi-Exchange Arbitrage Opportunities

- Risk Management Considerations

- Technical Infrastructure Requirements

- Data Collection and Processing

- Computational Optimization Techniques

- Advanced Techniques and Edge Cases

- Machine Learning Enhancement

- Microstructure Noise Filtering

- Regulatory and Compliance Considerations

- Case Studies and Performance Analysis

- Historical Performance During Market Events

- Backtesting Methodology and Results

- Live Trading Considerations

- Integration with Other Trading Methodologies

- Combining with Technical Analysis

- On-Chain Analytics Integration

- Sentiment Analysis Correlation

- Future Developments and Emerging Trends

- Decentralized Exchange Order Books

- Cross-Chain Order Book Aggregation

- Artificial Intelligence and Predictive Modeling

- Conclusion: Mastering the Hidden Dynamics of Cryptocurrency Markets

The Anatomy of Cryptocurrency Order Books

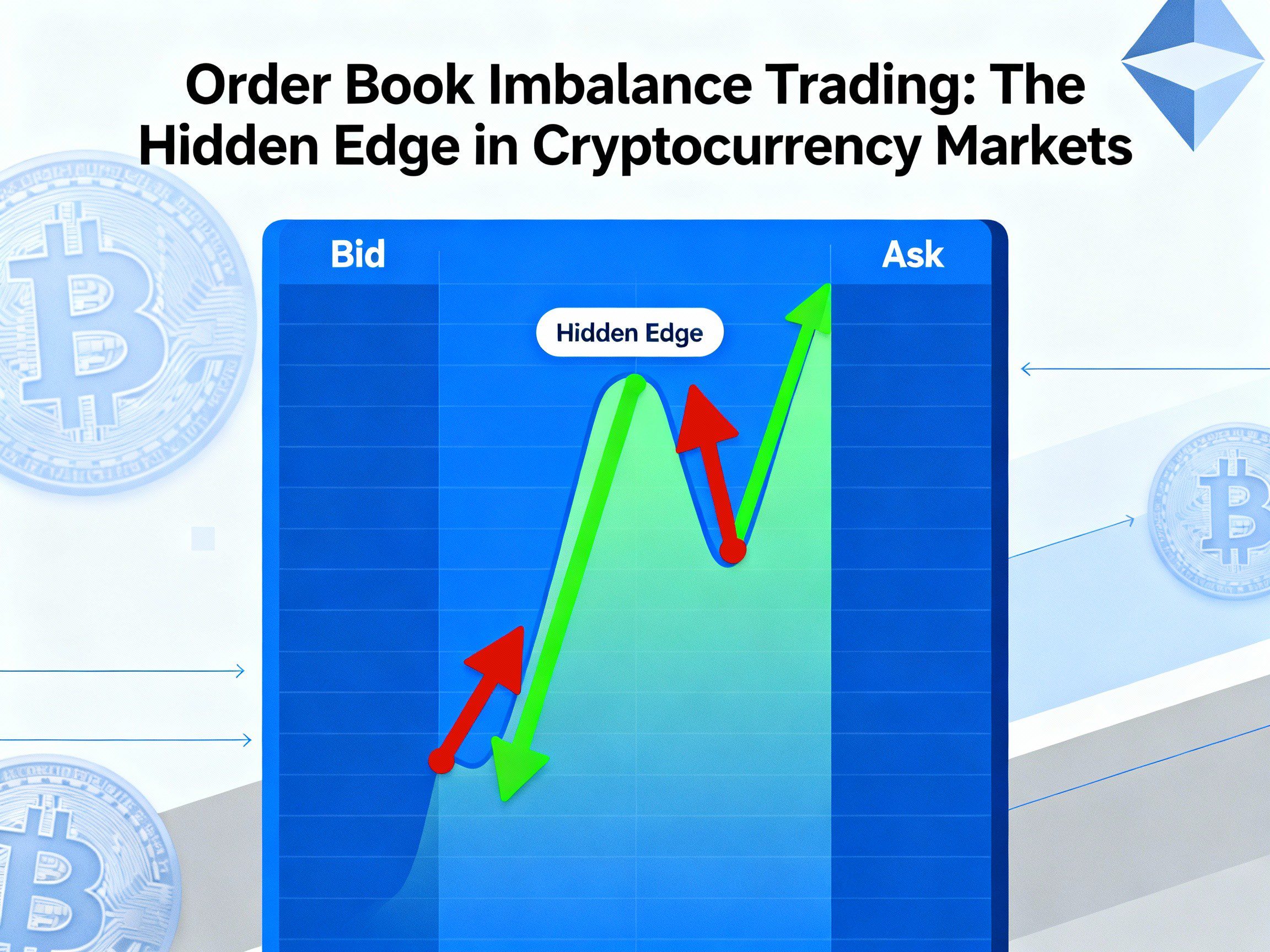

An order book serves as the central nervous system of any cryptocurrency exchange, displaying all pending buy and sell orders at different price levels. Think of it as a real-time snapshot of market sentiment, where every limit order represents a trader’s conviction about future price direction.

The order book consists of two primary components: the bid side (buy orders) and the ask side (sell orders). Each side contains multiple price levels, with each level showing the total volume of orders waiting to be executed at that specific price. The gap between the highest bid and lowest ask creates what we call the spread—a crucial metric that reflects market liquidity and trading costs.

Table 1: Sample Order Book Structure for BTC/USDT

| Bid Price | Bid Volume | Ask Price | Ask Volume |

|---|---|---|---|

| $43,250 | 2.45 BTC | $43,255 | 1.82 BTC |

| $43,249 | 3.21 BTC | $43,256 | 2.93 BTC |

| $43,248 | 1.87 BTC | $43,257 | 4.15 BTC |

| $43,247 | 5.63 BTC | $43,258 | 3.27 BTC |

| $43,246 | 4.92 BTC | $43,259 | 2.51 BTC |

Depth Visualization and Market Psychology

The depth of an order book—referring to the cumulative volume at various price levels—provides insights into potential support and resistance zones. When you visualize this depth, you begin to see patterns that price charts alone cannot reveal. Large clusters of orders at specific price points often act as psychological barriers, influencing how price moves through these levels.

Consider how institutional traders place their orders: they rarely execute large trades at market prices. Instead, they strategically position limit orders at levels where they expect price reversals or continuations. By learning to read these patterns, individual traders can align their strategies with institutional order flow, essentially “following the smart money.”

Defining and Measuring Order Book Imbalance

The Mathematics of Imbalance

Order book imbalance quantifies the asymmetry between buy and sell orders at any given moment. The simplest calculation involves comparing the total bid volume against the total ask volume within a specified price range or depth level.

The basic imbalance ratio can be expressed as:

Imbalance Ratio = (Bid Volume – Ask Volume) / (Bid Volume + Ask Volume)

This ratio ranges from -1 to +1, where positive values indicate buying pressure and negative values suggest selling pressure. However, this simple calculation only scratches the surface of what order book analysis can reveal.

Advanced Imbalance Metrics

Professional traders employ more sophisticated metrics that weight orders based on their proximity to the current price. Orders placed closer to the market price carry more significance because they’re more likely to be executed in the near term. This understanding leads us to the Volume-Weighted Order Book Imbalance (VWOI):

Table 2: Volume-Weighted Imbalance Calculation Example

| Distance from Mid-Price | Weight | Bid Volume | Weighted Bid | Ask Volume | Weighted Ask |

|---|---|---|---|---|---|

| 0.1% | 1.0 | 5.2 BTC | 5.20 | 3.8 BTC | 3.80 |

| 0.2% | 0.8 | 4.7 BTC | 3.76 | 5.1 BTC | 4.08 |

| 0.3% | 0.6 | 6.3 BTC | 3.78 | 4.2 BTC | 2.52 |

| 0.4% | 0.4 | 3.9 BTC | 1.56 | 7.5 BTC | 3.00 |

| 0.5% | 0.2 | 8.1 BTC | 1.62 | 6.8 BTC | 1.36 |

| Total | 15.92 | 14.76 |

In this example, the volume-weighted imbalance would be: (15.92 – 14.76) / (15.92 + 14.76) = 0.038, indicating slight buying pressure.

Temporal Dynamics of Imbalance

Order book imbalance isn’t static—it fluctuates continuously as traders add, modify, and cancel their orders. These dynamics create patterns that experienced traders learn to recognize. Sudden shifts in imbalance often precede price movements, particularly when accompanied by changes in order book depth at key price levels.

Understanding these temporal patterns requires analyzing how imbalance evolves over different time frames. Short-term imbalances (measured in seconds or minutes) might indicate immediate price pressure, while longer-term imbalances (hours or days) can reveal accumulation or distribution phases.

Implementing Order Book Imbalance Strategies

Strategy Development Framework

Developing a successful order book imbalance strategy requires a systematic approach that combines data analysis, risk management, and execution optimization. The process begins with defining clear entry and exit signals based on imbalance thresholds and confirming indicators.

Consider starting with a simple momentum-based approach: when the order book shows sustained buying imbalance above a certain threshold (for example, +0.3), combined with increasing bid depth near the current price, this might signal an upcoming price increase. Conversely, selling imbalance below -0.3 with growing ask-side pressure could indicate an impending decline.

Real-Time Signal Generation

The key to successful implementation lies in processing order book data in real-time and generating actionable signals quickly enough to capitalize on short-term opportunities. This involves:

Table 3: Signal Generation Parameters

| Parameter | Description | Typical Range | Optimization Notes |

|---|---|---|---|

| Imbalance Threshold | Minimum imbalance to trigger signal | 0.2 – 0.5 | Higher for volatile markets |

| Depth Level | Price range for calculation | 0.5% – 2% | Wider for less liquid pairs |

| Time Window | Period for averaging | 10s – 5min | Shorter for scalping |

| Volume Filter | Minimum order size to include | $100 – $10,000 | Adjust based on market cap |

| Confirmation Period | Time to maintain imbalance | 3 – 10 intervals | Longer reduces false signals |

Multi-Exchange Arbitrage Opportunities

One particularly profitable application involves monitoring order book imbalances across multiple exchanges simultaneously. When Binance shows strong buying pressure while Coinbase displays selling pressure for the same cryptocurrency pair, this divergence often creates arbitrage opportunities.

These cross-exchange imbalances typically arise from differences in user bases, regional preferences, or temporary liquidity disparities. Traders equipped with proper infrastructure can execute trades on both exchanges simultaneously, profiting from the price convergence that usually follows.

Risk Management Considerations

Order book data can be manipulated through spoofing—the practice of placing large orders with no intention of execution. To mitigate this risk, successful traders incorporate several defensive measures into their strategies:

First, they filter out orders that appear and disappear rapidly, focusing instead on orders that remain in the book for meaningful periods. Second, they combine order book signals with other indicators like actual trade flow, on-chain metrics from sources like Glassnode, or sentiment analysis to confirm the authenticity of apparent imbalances.

Technical Infrastructure Requirements

Data Collection and Processing

Implementing order book imbalance strategies demands robust technical infrastructure capable of handling high-frequency data streams. Most cryptocurrency exchanges provide WebSocket APIs that stream order book updates in real-time, but processing these streams efficiently requires careful system design.

The data pipeline typically consists of several components working in harmony. A connection manager maintains stable WebSocket connections to multiple exchanges, handling reconnections and error recovery automatically. The incoming data feeds into a normalized processing layer that standardizes order book formats across different exchanges, making cross-exchange analysis possible.

Table 4: Technical Infrastructure Components

| Component | Function | Technology Options | Performance Requirements |

|---|---|---|---|

| Data Ingestion | WebSocket connection management | Python asyncio, Node.js, Go | <10ms latency |

| Message Queue | Buffer and distribute updates | Redis, Kafka, RabbitMQ | 100k+ msg/sec |

| Processing Engine | Calculate imbalances | C++, Rust, Java | <1ms per calculation |

| Database | Store historical data | TimescaleDB, InfluxDB | 1M+ writes/sec |

| Execution Gateway | Send orders to exchanges | FIX protocol, REST APIs | <50ms round-trip |

Computational Optimization Techniques

Processing order book data at scale requires careful optimization. Simple improvements like using numpy arrays instead of Python lists for numerical calculations can reduce processing time by orders of magnitude. More advanced optimizations might involve implementing critical calculations in compiled languages or utilizing GPU acceleration for parallel processing of multiple trading pairs.

Memory management becomes crucial when maintaining real-time order books for dozens of trading pairs across multiple exchanges. Efficient data structures like red-black trees or skip lists allow for fast order insertion and deletion while maintaining sorted order—essential for accurate order book reconstruction from update streams.

Advanced Techniques and Edge Cases

Machine Learning Enhancement

While traditional rule-based approaches to order book imbalance trading can be effective, machine learning techniques offer opportunities for discovering non-obvious patterns and relationships. Random forests and gradient boosting models can identify complex interactions between multiple order book features that human traders might miss.

Consider training a model on historical order book snapshots, using features like imbalance at multiple depth levels, rate of change in imbalance, order size distributions, and spread dynamics. The target variable might be the price movement over the next minute or the probability of a significant price change. Platforms like TensorFlow or scikit-learn provide the tools necessary for developing these models.

However, machine learning in this context requires careful consideration of data quality and model validation. Order book dynamics can change dramatically during different market regimes, so models trained on bull market data might perform poorly during corrections or sideways markets.

Microstructure Noise Filtering

Order books contain significant noise from high-frequency trading algorithms, market makers, and small retail orders. Filtering this noise while preserving meaningful signals represents a fundamental challenge in order book analysis.

One effective approach involves applying exponential moving averages to imbalance measurements, smoothing out short-term fluctuations while maintaining responsiveness to genuine shifts in market sentiment. Another technique uses order size filtering, focusing only on orders above a certain threshold that likely represent institutional activity rather than algorithmic noise.

Table 5: Noise Filtering Techniques

| Technique | Application | Advantages | Disadvantages |

|---|---|---|---|

| EMA Smoothing | Time-series filtering | Simple, low latency | Lag in signal detection |

| Median Filtering | Outlier removal | Robust to manipulation | Computationally intensive |

| Kalman Filtering | State estimation | Optimal for linear systems | Complex parameter tuning |

| Wavelet Denoising | Multi-scale analysis | Preserves sharp features | Requires expertise |

| Order Size Filtering | Focus on large orders | Reduces noise significantly | May miss retail momentum |

Regulatory and Compliance Considerations

As order book trading strategies become more sophisticated, traders must navigate an evolving regulatory landscape. Different jurisdictions have varying rules about market manipulation, particularly regarding practices that might resemble spoofing or layering. Understanding these regulations is crucial for developing compliant trading strategies.

In the United States, the CFTC has provided guidance on algorithmic trading in cryptocurrency markets. European traders must consider MiFID II requirements, even though cryptocurrencies remain largely unregulated. Always consult with legal professionals familiar with your jurisdiction’s specific requirements.

Case Studies and Performance Analysis

Historical Performance During Market Events

Examining how order book imbalance strategies performed during significant market events provides valuable insights into their robustness and limitations. During the March 2020 COVID-19 crash, order book imbalances provided early warning signals hours before the cascade of liquidations that drove prices down dramatically.

In that instance, persistent selling pressure appeared in order books across major exchanges, with ask-side volume overwhelming bids by ratios exceeding 3:1 at times. Traders who recognized these signals and either exited positions or established shorts before the crash avoided significant losses or profited from the decline.

Conversely, during the bull run of late 2020 and early 2021, order book imbalances often showed sustained buying pressure that preceded major upward movements. The key difference during trending markets versus ranging markets lies in the persistence of imbalances—trends show sustained directional imbalance, while ranges exhibit oscillating imbalances around equilibrium.

Backtesting Methodology and Results

Properly backtesting order book strategies presents unique challenges because historical order book data is massive and expensive to store. A single day of full order book data for a major cryptocurrency pair can exceed several gigabytes, making comprehensive backtesting computationally intensive.

Despite these challenges, rigorous backtesting remains essential for strategy validation. A well-designed backtest should account for realistic execution assumptions, including slippage, exchange fees, and the market impact of your own orders. Tools like Freqtrade or custom backtesting frameworks can help simulate these real-world constraints.

Table 6: Sample Backtest Results (BTC/USDT, 2023)

| Strategy Variant | Win Rate | Avg Win/Loss | Sharpe Ratio | Max Drawdown | Annual Return |

|---|---|---|---|---|---|

| Simple Imbalance | 54% | 1.15 | 1.23 | -12% | +28% |

| Weighted Imbalance | 57% | 1.22 | 1.45 | -10% | +34% |

| ML-Enhanced | 61% | 1.31 | 1.78 | -8% | +42% |

| Multi-Exchange | 59% | 1.18 | 1.92 | -7% | +38% |

| Filtered Composite | 56% | 1.28 | 1.65 | -9% | +36% |

Live Trading Considerations

Transitioning from backtesting to live trading requires careful consideration of additional factors. Order book dynamics in live markets include elements that historical data cannot capture, such as your own market impact and the adaptive behavior of other algorithmic traders.

Start with small position sizes to validate that your strategy performs as expected in live conditions. Monitor key metrics like fill rates, slippage, and execution times to ensure they align with backtested assumptions. Many successful traders maintain parallel paper trading systems that run continuously alongside live strategies, providing ongoing validation and alerting to any performance divergences.

Integration with Other Trading Methodologies

Combining with Technical Analysis

Order book imbalance strategies gain considerable power when combined with traditional technical analysis. Support and resistance levels identified through price action analysis often correspond with significant order clusters in the book, providing confluence for trading decisions.

For instance, when price approaches a major resistance level identified on the daily chart, monitoring order book dynamics at that level reveals whether sellers are indeed defending that price point or if buying pressure might push through. This multi-dimensional analysis reduces false signals and increases confidence in trade execution.

On-Chain Analytics Integration

The transparency of blockchain technology allows traders to combine order book analysis with on-chain metrics for even deeper market insights. When order books show accumulation patterns while on-chain data from providers like CryptoQuant indicates decreasing exchange balances, this confluence strongly suggests upward price pressure.

Similarly, tracking large wallet movements and correlating them with order book changes can reveal institutional positioning. If known institutional wallets move funds to exchanges while order books show increasing sell-side pressure, this might signal impending selling that retail traders can front-run.

Sentiment Analysis Correlation

Social sentiment from platforms like Twitter, Reddit, and Telegram often precedes order book changes, particularly in smaller cryptocurrency markets. By monitoring sentiment shifts and watching for corresponding order book adjustments, traders can position themselves ahead of retail-driven movements.

Advanced practitioners use natural language processing to quantify sentiment from social media and news sources, then correlate these metrics with order book imbalances. When sentiment turns strongly positive but order books show selling pressure, this divergence might indicate smart money distribution into retail euphoria—a classic topping pattern.

Future Developments and Emerging Trends

Decentralized Exchange Order Books

As decentralized exchanges (DEXs) evolve beyond simple automated market makers (AMMs) to include order book functionality, new opportunities emerge for imbalance trading. Projects like dYdX and Serum already offer on-chain order books that provide transparency impossible in centralized systems.

These decentralized order books eliminate concerns about fake orders or hidden liquidity, as all orders exist on-chain and require gas fees to place or cancel. This added cost structure changes the dynamics of order book manipulation, potentially making imbalance signals more reliable.

Cross-Chain Order Book Aggregation

The fragmentation of liquidity across multiple blockchains creates opportunities for traders who can aggregate and analyze order books across different chains. As bridge technologies improve and cross-chain trading becomes more seamless, strategies that capitalize on imbalances between Ethereum-based DEXs and those on Solana, Binance Smart Chain, or other networks will become increasingly profitable.

Artificial Intelligence and Predictive Modeling

The next frontier in order book trading involves artificial intelligence systems that can process vast amounts of microstructure data in real-time and identify patterns humans cannot perceive. Deep learning models, particularly recurrent neural networks and transformer architectures, show promise in predicting short-term price movements based on order book dynamics.

These AI systems can simultaneously analyze order books across hundreds of trading pairs and exchanges, identifying correlations and leading indicators that inform trading decisions. As computational power becomes cheaper and models more sophisticated, AI-driven order book analysis will likely become the dominant approach for institutional traders.

Conclusion: Mastering the Hidden Dynamics of Cryptocurrency Markets

Order book imbalance trading represents a sophisticated approach to cryptocurrency markets that goes beyond surface-level price analysis to examine the underlying forces driving market movements. By understanding how to read, interpret, and act upon order book signals, traders gain access to information that remains hidden from those relying solely on price charts and traditional indicators.

The journey from understanding basic order book structure to implementing profitable imbalance strategies requires dedication to learning market microstructure, developing technical infrastructure, and maintaining disciplined risk management. However, for those willing to invest the time and resources, order book analysis offers a sustainable edge in increasingly efficient cryptocurrency markets.

As markets evolve and new technologies emerge, the fundamental principle behind order book trading remains constant: prices move based on the interaction between buyers and sellers, and order books provide the most direct window into this interaction. Whether trading manually or through sophisticated algorithms, understanding order book dynamics will continue to separate successful traders from the crowd.

The strategies and techniques discussed in this article provide a foundation for developing your own order book trading approach. Remember that successful trading requires continuous learning and adaptation. Markets evolve, new patterns emerge, and strategies that work today might need adjustment tomorrow. Stay curious, keep analyzing, and always maintain proper risk management as you explore the fascinating world of order book imbalance trading.

For those ready to begin their journey into order book analysis, start by observing order books on your preferred exchange during different market conditions. Notice how imbalances develop before significant moves, how fake orders appear and disappear, and how institutional players position their orders. With time and practice, these patterns will become second nature, providing you with a valuable edge in the competitive world of cryptocurrency trading.

The path to mastery in order book trading is challenging but rewarding. As you develop your skills and build your infrastructure, remember that every successful trader started exactly where you are now. The difference lies not in natural talent but in persistence, continuous learning, and disciplined application of knowledge. The cryptocurrency markets offer unprecedented opportunities for those willing to look beyond the obvious and understand the hidden dynamics that truly drive price discovery.